Maude Pugliese is an Associate Professor at the Institut national de la recherche scientifique (Université du Québec) in the Population Studies program and holds the Canada Research Chair in Family Financial Experiences and Wealth Inequality. She is also the scientific director of the Partenariat de recherche Familles en mouvance, which brings together dozens of researchers and practitioners to study the transformations of families and their repercussions in Quebec. In addition, she is the director of Observatoire des réalités familiales du Québec/Famili@, a knowledge mobilization organization that diffuses the most recent research on family issues in Quebec to a broad public in accessible terms. Her current research work focuses on the intergenerational transmission of wealth and of money management practices, gender inequalities in wealth and indebtedness, and how new intimate regimes (separation, repartnering, living apart together, polyamory, etc.) are transforming ideals and practices of wealth accumulation.

Topic: Finances

Research Snapshot: Living Arrangements and Housing Affordability Among Young Adults in Canada

Highlights of a study of how young newcomers are coping with housing unaffordability

Research Snapshot: Gaps in Employment Protections for Pregnant Migrants in Canada

Summary of a study on women who were pregnant or gave birth while having precarious immigration status

Research Snapshot: The Value and Distribution of Family Caregiving in Canada

A summary of a study about the economic value and distribution of caregiving

Research Snapshot: Housing Affordability and Homeownership Among Immigrant Families in Canada

Key findings from a study on immigrant families and housing

Infographic: Supporting Employed Caregivers Makes Good Business Sense

Research on Aging, Policies and Practice provides new data on the “business case” for supporting employed caregivers

Infographic: Employed Caregivers at Higher Risk of Negative Outcomes

Research on Aging, Policies and Practice has published new data on how caregiving affects employed Canadians.

Research Snapshot: Parenthood and the Gendered Impact of Job Loss

Highlights from a study about gendered consequences of job loss

Infographic: How Does Caregiving Impact Paid Work for Employed Women and Men?

Research on Aging, Policies and Practice has published new data on how caregiving affects employed Canadians.

Research Snapshot: Family Dynamics and the Canadian Gender Income Gap

A summary of research on families, gender equality, and income in Canada

In Brief: Productivity and Preferences While Working from Home

Diana Gerasimov shares recent insights on experiences of working from home.

COVID-19 IMPACTS: Retirees and Family Finances in Canada

Edward Ng, PhD

September 3, 2020

COVID-19 has had a major impact on the labour market, work–life and family finances in Canada. Amid the public health measures and economic lockdown, many organizations and businesses across the country rapidly laid off employees and/or transitioned employees to teleworking. As a result, the unemployment rate increased from 8% to 14% between March and May 2020, reaching the highest figure recorded since comparable data became available in 1976.1 A survey conducted April 10–12, 2020 by Leger, the Association for Canadians Studies (ACS) and the Vanier Institute found that more than one-third of Canadians aged 18 and older were financially impacted due to COVID-19 (i.e. lost their job temporarily or permanently, or experienced pay or income losses).2

Within many families, this context of uncertainty in the labour market can have a major impact on aspirations, such as buying a home, having a child3 or pursuing post-secondary education. Retirement has also been affected, with pre-retirees and retirees alike adapting and reacting to the evolving context to support family. Retired people are in a unique situation, however, when it comes to the financial impact of COVID-19, as they are not in the labour force, and those who are seniors have access to other income supports. As their capacity to provide financial support to family is shaped by their own finances, understanding their unique realities and experiences will help shed light on this aspect of COVID-19 impacts on families in Canada.

Retirement plans shaped by family finances and available supports

While a growing share of Canadians are working past their 50s and beyond the traditional retirement age of 65, the retired population has grown overall as population aging has continued. According to Statistics Canada, the average age at retirement for all workers in Canada was 64.3 in 2019. That said, many older Canadians continue to work well into their 60s and beyond. In 2017, nearly one-third of Canadians aged 60 and older said that they worked (or wanted to work) in the previous year, half (49%) of whom did so “out of necessity.”4

Prior to COVID-19, many Canadians expressed concern about their financial preparedness for retirement. According to the 2019 Canadian Financial Capability Survey, 69% of pre-retired Canadians are preparing financially for retirement, on their own or through a workplace pension plan.5 But more than one-third of surveyed Canadians aged 55 and older reported are concerned they don’t have enough savings (37%) and/or that they will be able to cover health care costs as they age (34%).6

Retirees who are seniors have access to income support through government pension payments, available to all Canadians at age 65 who have lived in the country for at least 10 years. On top of privately arranged retirement schemes and/or personal retirement savings or investments, public income programs for seniors, such as the Old Age Security (OAS) program, the Guaranteed Income Supplement (GIS) and the Canada/Quebec Pension Plan, provide senior retirees in Canada with fixed and relatively stable income sources that can help protect them against economic instability, such as the economic shock resulting from the COVID-19 pandemic.

In May 2020, in response to the financial stress placed on retirees and seniors, the federal government announced additional financial support for seniors as a one-time payment of $500 for individuals who receive both the OAS and the GIS to offset additional costs from COVID-19.7

Retiree investments impacted, but overall family finances less affected

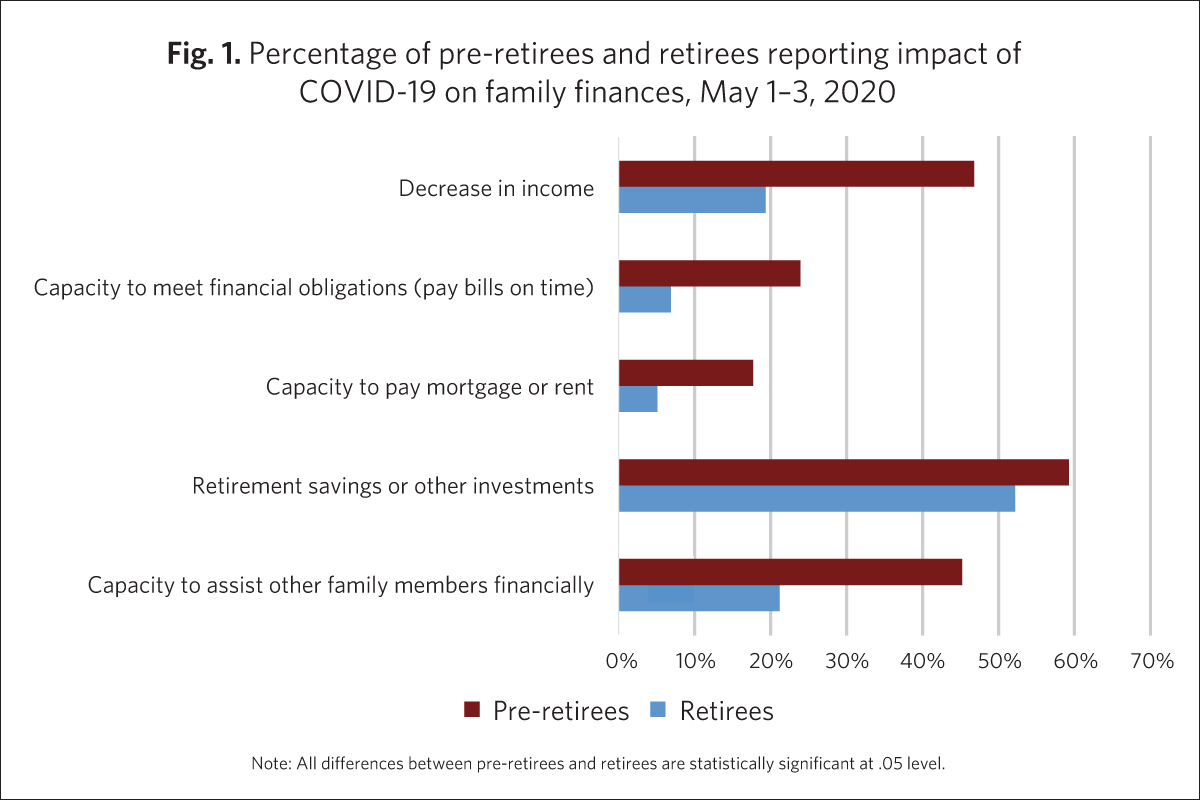

A survey conducted by the Leger, ACS and the Vanier Institute in early May provided one of the first glimpses into the pandemic’s financial impact on retirees.8 It showed that only 1 in 5 retirees9 reported a decrease in income as a result of the COVID-19 crisis, compared with close to one half of pre-retirees (47%) (fig. 1).

In fact, the polling data showed that some (7%) of retirees reported difficulty in their capacity to meet financial obligations, such as paying bills, compared with close to 1 in 4 pre-retirees (24%). Similarly, 1 in 20 (5%) retirees reported difficulty in paying mortgage or rent, compared with close to 1 in 5 pre-retirees (18%).

While retirees have access to public income support, many also have access to additional income support through savings or other investments. (In 2015, 50% of seniors in Canada reported receiving income from investments.)10 The COVID-19 outbreak resulted in financial market uncertainties and turbulences that added considerable stress on investors in general, and this is the area where retirees were most adversely affected. The polling data showed that more than half (52%) of retirees reported negative impact on their retirement savings or other investments – though the impact was greater among pre-retirees (59%).

Retirees assisting other family members financially

Family can be viewed as a potential source of insurance against abrupt financial shocks. Since some retirees were less exposed to the pandemic-related economic shocks, they have been a potential source of financial support for their children or younger family members, who may have been more adversely affected. A study on the impact of severe economic recessions found that, during the 2008 financial crisis, 28% of households in the United States reported getting financial help from family and friends.11

How did COVID-19 affect retirees’ ability to assist other family members in Canada? When asked, about 1 in 5 retirees (21%) reported that the pandemic had affected their ability to assist other family members financially. Among the pre-retirees, who were more exposed to the economic shock produced by COVID-19, the rate was 45%. Retirees who received income assistance from their children or grandchildren (some of whom could be pre-retirees) may therefore have also been indirectly affected in this way.

Retirement timing is being affected for one-third of surveyed Canadians

As families continue to navigate the impacts of COVID-19, data show that many workers are adapting their retirement plans. A recent US survey found that 39% of American workers are changing their retirement timing,12 primarily for financial reasons (e.g. they had to use some of their savings, some of their investments may have lost value during the pandemic, there is less certainty in general about how much money they will need in retirement).

A separate survey from Canada suggests a similar trend may be taking place in Canada, with one-third (33%) of adults who plan to retire saying that they will retire later than planned as a result of COVID-19.13 However, 8% of respondents said they would retire earlier than originally planned, possibly due to wanting to avoid continued uncertainty and turbulence in the labour market (if they are financially able to do so).

While it is too early to draw a clear picture of the diverse ways COVID-19 has impacted retirement in Canada, early data shows that retirees are less financially impacted on average, as pre-retirees seem to have been more exposed to the economic impacts. Nonetheless, surveys show that the increased uncertainty is having an impact on people’s retirement planning, and further research will be important to understanding how this is affecting family finances and well-being more generally.

Edward Ng, PhD, Vanier Institute on secondment from Statistics Canada

Notes

- Statistics Canada, “Labour Force Survey, May 2020,” The Daily (Ottawa: Statistics Canada, 2020). According to the Labour Force Survey, from February to April of 2020, 5.5 million Canadian workers were affected by the COVID-19 economic shutdown, which included a drop in employment of 3 million and a COVID-19-related increase in absences from work of 2.5 million. Link: https://bit.ly/3j99UfM.

- Ana Fostik and Jennifer Kaddatz, “Family Finances and Mental Health During the COVID‑19 Pandemic” (May 26, 2020).

- See Ana Fostik, “Uncertainty and Postponement: Pandemic Impact on Fertility in Canada,” The Vanier Institute of the Family (June 30, 2020).

- Myriam Hazel, “Reasons for Working at 60 and Beyond,” Labour Statistics at a Glance, Statistics Canada catalogue no. 71-222-X (December 14, 2018). Link: https://bit.ly/2SJqjxW.

- Financial Consumer Agency of Canada, Canadians and their Money: Key Findings from the 2019 Canadian Financial Capability Survey (November 2019). Link: https://bit.ly/34ypopw.

- RBC, 2017 RBC Financial Independence in Retirement Poll (February 14, 2017). Link: https://bit.ly/2Yyyxe6.

- Justin Trudeau, Prime Minister of Canada, “Prime Minister Announces Additional Support for Canadian Seniors,” Government of Canada (May 12, 2020). Link: https://bit.ly/308AUp2.

- The survey, conducted by the Vanier Institute of the Family, the Association for Canadian Studies and Leger on May 1–3, 2020, included approximately 1,500 individuals aged 18 and older, interviewed using computer-assisted web-interviewing technology in a web-based survey. Using data from the 2016 Census, results were weighted according to gender, age, mother tongue, region, education level and presence of children in the household in order to ensure a representative sample of the population. No margin of error can be associated with a non-probability sample (web panel in this case). However, for comparative purposes, a probability sample of 1,512 respondents would have a margin of error of ±2.52%, 19 times out of 20.

- Retirees are defined as those aged 45 and above who reported being retired in the polling survey, when asked about their current occupation. Pre-retirees are other respondents in the same age group who reported an occupation other than homemaker or a student. Since there is no mandatory retirement age in Canada, among those aged 45 and more, the polling data showed that some 4% of those aged 65 and above were still working, while some 29% of the retirees in the same age group were in fact younger than 65.

- Statistics Canada, “Income Sources and Taxes (16), Income Statistics (4) in Constant (2015) Dollars, Age (9), Sex (3) and Year (2) for the Population Aged 15 Years and Over in Private Households of Canada, Provinces and Territories, Census Metropolitan Areas and Census Agglomerations, 2006 Census – 20% Sample Data and 2016 Census – 100% Data,” Data Tables, 2016 Census (September 12, 2017). Link: http://bit.ly/2i6MVUR.

- National Research Council, “Assessing the Impact of Severe Economic Recession on the Elderly: Summary of a Workshop” (Washington, DC: The National Academies Press, 2011). Link: https://bit.ly/2X8b9mU.

- Edward Jones Canada, The Four Pillars of the New Retirement (June 25, 2020).

- Ibid.

Food Insecurity and Family Finances During the Pandemic

Nadine Badets

June 12, 2020

The COVID‑19 lockdown and ensuing economic repercussions have created a significant amount of financial stress for families in Canada. Between February and April 2020, about 1.3 million people in Canada were unemployed, with approximately 97% of the newly unemployed on temporary layoff, meaning they expect to go back to their jobs once the pandemic restrictions are relaxed.1

Research has shown that financial insecurity can severely limit access to food for low income families and exacerbate socio-economic inequities.2 Other factors, such as health and disability status, level of social support and the limited availability of certain food products, also contribute to food insecurity during the COVID‑19 pandemic.

Financial inequities intensified during physical distancing and economic lockdown

Overall, 5.5 million adults in Canada have either been affected by job loss or reduced work hours during the COVID-19 lockdown, meaning these people and their households have a significant reduction in income for necessities such as food and shelter.3 In 2018, about 3.2 million people lived below Canada’s official poverty line,4 and the economic impacts of the pandemic have likely increased these numbers.

The pandemic is also amplifying existing financial inequities.5 In Canada in 2015, the national prevalence of low income was 14%, however it was much higher among some groups, such as immigrants (Arab, West Asian, Korean, Chinese), Indigenous Peoples (First Nations people, Inuit, Métis), and Black people.6, 7 These groups were more likely to be living with low income before the COVID‑19 lockdown, and have been more likely than others to report that the pandemic has had a negative effect on their finances. According to recent survey data from the Vanier Institute of the Family, the Association of Canadian Studies and Leger,8 over half of visible minorities (51%) had a decrease in their income during the lockdown, and Indigenous peoples (42%) were most likely to report having difficulty meeting financial obligations, such as being able to pay bills on time.9, 10

Food banks across Canada have seen surges in use since the beginning of the COVID‑19 pandemic

Prior to the COVID‑19 pandemic, Food Banks Canada estimated that food bank use across the country had stabilized, with 2019 having almost the same number of visits as 2018, remaining at levels similar to 2010. In the month of March 2019, there were close to 1.1 million visits to food banks across Canada, with more than 374,000 visits for feeding children.11

Statistics Canada estimates that in 2017–2018 about 9% of households (1.2 million) in Canada were food insecure, meaning they struggled financially to get food and did not have enough for all household members to eat regular and nutritious meals.12, 13 As with financial insecurity, food insecurity disproportionately affects certain population groups in Canada. For example, in 2014 food insecurity among Black people (29%) and Indigenous people (26%) was more than double the national average (12%).14

Research has consistently found that people living in remote and Northern communities are more likely to experience food insecurity, such as Inuit communities in Inuit Nunangat, the Inuit homeland.15 It has also been found that Indigenous populations living in urban areas experience high levels of food insecurity. In 2017, 38% of Indigenous peoples 18 years and older living in urban areas were food insecure.16

Since the COVID‑19 pandemic started, Food Banks Canada reported that there has been an average increase of 20% in demand for services from food banks across the country, alarmingly close to the 28% increase seen during the Great Recession. Projections by Food Banks Canada estimate that demand could continue to rise to between 30% and 40% higher than pre-pandemic levels. Some food banks – such as The Daily Bread in Toronto, one of the largest food banks in Canada – have seen increases of over 50% in use.17

Increases in grocery sales associated with the receipt of financial support through CERB

Early in the pandemic (late March to early April 2020), 63% of people reported that they stocked up on essential groceries and pharmacy products as a precaution.18

Grocery sales across Canada saw a sharp increase in March 2020, rising 40% toward the end of the month and continued to remain high in mid‑April.19 The delivery of federal financial supports for unemployed people, such as the Canadian Emergency Response Benefit (CERB),20 appear to be directly linked with an increase in grocery sales, which is likely helping to mitigate food insecurity for some Canadians.21

However, CERB currently only allows recipients to claim the benefit four times for a total of 16 weeks. As July 2020 approaches, many Canadians will be using up their final installment of CERB, and not all will be eligible to be transferred to EI, which could have a serious impact on food insecurity in Canada.

Single parents and seniors with low levels of social support struggle the most to get groceries

Physical (social) distancing measures have also created new barriers for individuals and families trying to navigate new rules of when, how and with whom they can or should buy groceries. For some, such as seniors, single parents, people with disabilities and those who have (or are caring for someone with) compromised immune systems, having limited finances and little social support can seriously restrict access to food.

In 2017–2018, single parents with children under 18 years reported the highest levels of food insecurity in Canada. Female single parents had the highest rate of food insecurity at 25%, followed by male single parents at 16%.22 This compares with 12% among men and women living alone, 7% of couples with children under 18, and 3% of couples without children.23

Physical distancing measures can be particularly complex for single parents without access to child care, who may have to decide between bringing children to grocery stores, thereby breaking physical distancing rules and potentially exposing children to the virus, or turning to organizations like food banks for support.24

Seniors living with low income are less likely to have a high level of social support (77%) compared with seniors living in high income (89%). In periods of isolation such as the current lockdown, access to essentials like food can be challenging, especially for low income seniors who are ill, concerned for their health or unable to get groceries on their own due to physical or financial restrictions.25

Hoarding of certain foods limits supply and access for low income families and food banks

The COVID‑19 pandemic brought a series of panic-buying trends around the world, most notably of hand sanitizer and toilet paper.26 Many grocery stores and pharmacies have had their stock of certain food items depleted several times during the pandemic.

In mid-March 2020, sales of dry and canned foods in Canada surpassed those of fresh and frozen foods. Rice sales rose 239% compared with the same period in 2019, sales of pasta rose by 205%, canned vegetables by 180% and sales of infant formula by 103%.27 Shelf-stable foods such as these are usually a major part of food bank products,28 but are more difficult to come by during the pandemic and thus limit supplies for food insecure families.29

More research is needed to better understand the effects of the pandemic on hunger, nutrition and food insecurity in households across Canada in order to support and develop programs aimed at reducing inequities in access to food.

To find a food bank nearby or make a donation, visit the Food Banks Canada website.

Nadine Badets, Vanier Institute on secondment from Statistics Canada

Notes

- Statistics Canada, “COVID‑19 and the Labour Market in April 2020,” Infographics (May 8, 2020). Link: https://bit.ly/3duO2si.

- Visit the PROOF Food Insecurity Policy Research website for more on food insecurity and social inequities. Link: https://bit.ly/2MQH8T8.

- Statistics Canada, “COVID‑19 and the Labour Market in April 2020.”

- Statistics Canada, “Health and Social Challenges Associated with the COVID‑19 Situation in Canada,” The Daily (April 6, 2020). Link: https://bit.ly/3fErrvo.

- Learn about the impact of the COVID-19 pandemic on inequalities in Canada, see Canadian Human Rights Commission, Statement – Inequality Amplified by COVID-19 Crisis (March 31, 2020).

- Statistics Canada, “Visible Minority (15), Income Statistics (17), Generation Status (4), Age (10) and Sex (3) for the Population Aged 15 Years and Over in Private Households of Canada, Provinces and Territories, Census Metropolitan Areas and Census Agglomerations, 2016 Census – 25% Sample Data,” Data Tables, 2016 Census (updated June 17, 2019). Link: https://bit.ly/30OqUC2.

- Statistics Canada, “Aboriginal Identity (9), Income Statistics (17), Registered or Treaty Indian Status (3), Age (9) and Sex (3) for the Population Aged 15 Years and Over in Private Households of Canada, Provinces and Territories, Census Metropolitan Areas and Census Agglomerations, 2016 Census – 25% Sample Data,” Data Tables, 2016 Census (updated June 17, 2019). Link: https://bit.ly/2zPHMxb.

- The survey, conducted by the Vanier Institute of the Family, the Association for Canadian Studies and Leger, on March 10–13, March 27–29, April 3–5, April 10–12, April 17–19, April 24–26, May 1–3 and May 8–10, 2020, included approximately 1,500 individuals aged 18 and older, interviewed using computer-assisted web-interviewing technology in a web-based survey. All samples, with the exception of those from March 10–13 and April 24–26, also included booster samples of approximately 500 immigrants. In addition, from about May 1 to 10, there was an oversample of 450 Indigenous peoples. Using data from the 2016 Census, results were weighted according to gender, age, mother tongue, region, education level and presence of children in the household in order to ensure a representative sample of the population. No margin of error can be associated with a non-probability sample (web panel in this case). However, for comparative purposes, a probability sample of 1,512 respondents would have a margin of error of ±2.52%, 19 times out of 20.

- It is important to emphasize that there is a great deal of diversity within visible minority groups and Indigenous populations, all groups have unique and distinct experiences of financial and food insecurity, as well as histories, geographies, cultures, traditions, and languages.

- For more on the impact of the COVID-10 pandemic on immigrant families and First Nations people, Métis and Inuit, see Laetitia Martin, Families New to Canada and Financial Well-being During Pandemic (May 21, 2020) and Statistics Canada, “First Nations people, Métis and Inuit and COVID-19: Health and social characteristics,” The Daily (April 17, 2020). Link: https://bit.ly/2Y714r3.

- Food Banks Canada, “Hunger Count 2019.” Link: https://bit.ly/2AZ1GpP.

- Ibid.

- Statistics Canada, “Household Food Security by Living Arrangement,” Table 13-10-0385-01 (accessed May 27, 2020). Link: https://bit.ly/37iQDnq.

- Health Canada, Household Food Insecurity in Canada: Overview (page last updated February 18, 2020). Link: https://bit.ly/30JLCDh.

- Valerie Tarasuk, Andy Mitchell and Naomi Dachner, “Household Food Insecurity in Canada, 2014,” PROOF Food Insecurity Policy Research (updated May 12, 2017). Link: https://bit.ly/3eJ0mpl (PDF).

- Paula Arriagada, “Food Insecurity Among Inuit Living in Inuit Nunangat,” Insights on Canadian Society, Statistics Canada catalogue no. 75-006-X (February 1, 2017). Link: https://bit.ly/2maW9oN.

- Paula Arriagada, Tara Hahmann and Vivian O’Donnell, “Indigenous People in Urban Areas: Vulnerabilities to the Socioeconomic Impacts of COVID‑19,” STATCAN COVID‑19: Data to Insights for a Better Canada (May 26, 2020). Link: https://bit.ly/2zuTgWT.

- Beatrice Britneff, “Food Banks’ Demand Surges Amid COVID‑19. Now They Worry About Long-Term Pressures,” Global News (April 15, 2020). Link: https://bit.ly/3boEHRe.

- Statistics Canada, “How Are Canadians Coping with the COVID‑19 Situation?,” Infographic (April 8, 2020). Link: https://bit.ly/2WKdx21.

- Statistics Canada, “Study: Canadian Consumers Adapt to COVID‑19: A Look at Canadian Grocery Sales Up to April 11,” The Daily (May 11, 2020). Link: https://bit.ly/3cj58Jz.

- In April 2020, Canada’s federal government established the Canada Emergency Response Benefit (CERB), which provides $2,000 every four weeks to workers who have lost their income as a result of the pandemic. This benefit covers those who have lost their job, are sick, quarantined, or taking care of someone who is sick with COVID‑19. It applies to wage earners, contract workers and self-employed individuals who are unable to work. The benefit also allows individuals to earn up to $1,000 per month while collecting CERB. As a result of school and child care closures across Canada, the CERB is available to working parents who must stay home without pay to care for their children until schools and child care can safely reopen and welcome back children of all ages. Government of Canada, “Canada’s COVID-19 Economic Response Plan.” Link: https://bit.ly/2AhY1DD.

- Statistics Canada, “Study: Canadian Consumers Adapt to COVID‑19: A Look at Canadian Grocery Sales Up to April 11.”

- Statistics Canada, “Household Food Security by Living Arrangement.”

- Ibid.

- Ottawa Food Bank, “COVID‑19 Response Webinar – The First 5 Weeks” (May 13, 2020). Link: https://bit.ly/2AWXF55.

- Kristyn Frank, “COVID‑19 and Social Support for Seniors: Do Seniors Have People They Can Depend on During Difficult Times?,” StatCan COVID‑19: Data to Insights for a Better Canada (April 30, 2020). Link: https://bit.ly/3biLMmp.

- Statistics Canada, “Canadian Consumers Prepare for COVID‑19,” Price Analytical Series (April 8, 2020). Link: https://bit.ly/2WO1r86.

- Ibid.

- Food Banks Canada, “Support Your Local Food Bank.” Link: https://bit.ly/3gqmYwG.

Family Finances and Mental Health During the COVID‑19 Pandemic

Ana Fostik, PhD, and Jennifer Kaddatz

May 26, 2020

In March 2020, the coronavirus pandemic suddenly brought social and economic activities to a halt across Canada, with data showing serious impacts on labour market activity. Recent estimates from Statistics Canada show that 1 million fewer Canadians were employed in March than in February, and the usual labour market activity of 3.1 million Canadians was affected (i.e. worked fewer hours or lost their job).1

According to survey data for April 10–12, 2020 from the Vanier Institute of the Family, the Association for Canadian Studies (ACS) and Leger,2 38% of men and 34% of women aged 18 and older said that they lost their job temporarily or permanently, or experienced pay or income losses, due to the COVID-19 pandemic. Consequently, 27% of men and 25% of women reported a negative financial impact (i.e. ability to pay mortgage or rent and/or their bills).

Not surprisingly, Statistics Canada recently found that adults who suffered a major or moderate impact of the pandemic were much more likely to report fair or poor mental health than those who were less impacted (25% and 13%, respectively).3

Data collected in mid-April by the Vanier Institute of the Family, the Association for Canadian Studies and Leger show that younger adults have been particularly affected: more than half (52%) of those aged 18–34 reported a negative impact on their labour market activity (job or pay/income losses), compared with 39% of those aged 35–54 and 21% of those aged 55 and older. This is reflected in the shares of adults experiencing immediate negative financial outcomes, which were reported by 33% of adults under 55 and 15% of those over 55.

Adults in financial difficulty are more likely to report mental health issues

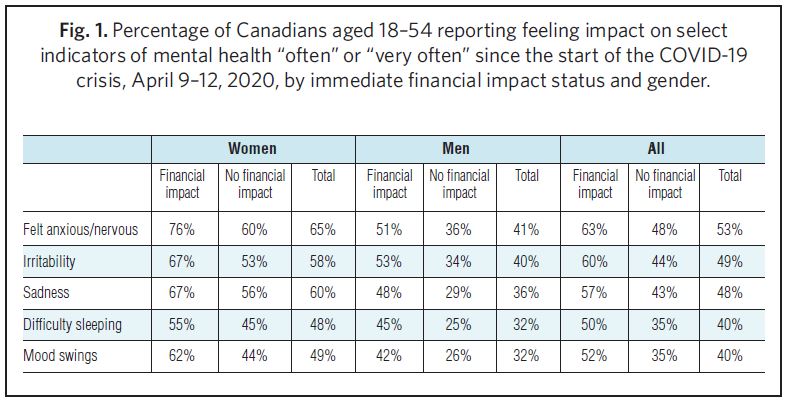

Among the core working age population (aged 18–54), just over half reported feeling anxious or nervous (53%), irritable (49%) or sad (48%) often or very often during the COVID-19 pandemic, according to the Vanier Institute/ACS/Leger survey. Four in 10 reported difficulty sleeping (40%) and having mood swings (40%) often or very often.

Among those who experienced immediate negative outcomes, such as not being able to pay rent or mortgage and/or their bills, about 6 in 10 reported anxiety or nervousness (63%), irritability (60%) or sadness (57%) often or very often, whereas half said they have had difficulty sleeping (50%) or experience mood swings (52%) often or very often (fig. 1).

Women in financial difficulty suffer from mental health issues in higher shares than men

According to the 2018 Canadian Community Health Survey, women were slightly less likely than men to report excellent/good mental health (66% and 71%, respectively).4 During the coronavirus pandemic, however, Statistics Canada found a much larger difference, at 49% of women and 60% of men.5

Vanier Institute/ACS/Leger survey data show women aged 18–54 reporting specific mental health issues often or very often in much larger shares than men of the same age. About 6 in 10 women reported experiencing anxiety or nervousness, irritability or sadness often or very often, compared with 4 in 10 men. Similarly, about half women experienced difficulty sleeping or mood swings often or very often, compared with 3 in 10 men (fig. 1).

This difference by gender in reporting mental health issues is maintained even when examining the proportions of men and women who suffered immediate negative financial outcomes and those who did not. For instance, three-quarters of women (76%), compared with half of men (51%), who had difficulty paying mortgage or rent and/or their bills reported feeling nervous or anxious often or very often. Almost 7 in 10 women in financial difficulty experience irritability (67%) or sadness (67%), compared with about half of men in the same situation (53% and 48%, respectively) (fig. 1).

About 6 in 10 of women in financial difficulty (55% and 62%) suffered difficulty sleeping and had mood swings often or very often, compared with 4 in 10 men in the same situation (45% and 42%, respectively) (fig. 1).

Adults with financial difficulties report similar mental health issues, whether living with young children or not

If women are significantly less likely than men to report positive mental health during the pandemic, even when financial outcomes are controlled for, what factors might be at play in creating these gender differences? Could these mental health challenges be related to family responsibilities?

An analysis of the April 10–12, 2020 data indicates that heightened symptoms of poor mental health do not appear to be linked to the presence of children in the home. Women who live with children aged 12 and younger in the household report experiencing anxiety (69%), irritability (60%), sadness (59%), difficulty sleeping (51%) and mood swings (51%) often and very often in similar proportions as women who do not live with children (63%, 57%, 60%, 47% and 48%, respectively). Men who live with young children also report these problems in similar proportions as those who do not (fig. 2).

Among women in financial difficulty, there is little difference in the share reporting any of these mental health problems whether they have young children living in the household or not. This is also true among women who did not experience immediate negative financial outcomes: living with children aged 12 and under in the household does not appear to make a difference (fig. 2).

Analysis of self-reported mental health status shows that some of the differences by gender persist when controlling for province of residence, age, financial difficulty, job/pay loss, presence of children aged 12 and under, household income, marital status and educational attainment. Controlling by these variables and compared with men who are in financial difficulty, women in financial difficulty are about twice as likely to suffer from anxiety, sadness or mood swings. Among adults who have not suffered financial negative outcomes, there are no significant differences between men and women in mental health outcomes once controlling for these factors.

While this analysis could not pinpoint potential reasons why women are more likely than men to report poor mental health symptoms, future research may seek to focus on psychological differences between women and men in crisis situations in order to determine whether or not women and men react differently in crisis situations or when there is an immediate threat to personal or family health and well-being. More research on the impact of gendered aspects of household work and caregiving, including the mental burden associated with these types of unpaid work, might also shed light on these differences.

Ana Fostik, PhD, Vanier Institute on secondment from Statistics Canada

Jennifer Kaddatz, Vanier Institute on secondment from Statistics Canada

Notes

- Statistics Canada, “The Impact of COVID-19 on the Canadian Labour Market,” Infographics (April 9, 2020). Link: https://bit.ly/3geJKro.

- A survey by the Vanier Institute of the Family, the Association for Canadian Studies and Leger, conducted March 10–13, March 27–29, April 3–5, April 10–12, April 17–19 and April 24–26, included approximately 1,500 individuals aged 18 and older, interviewed using computer-assisted web-interviewing technology in a web-based survey. All samples, except for the March 10–13 and April 24–26 samples, also included booster samples of approximately 500 immigrants. Using data from the 2016 Census, results were weighted according to gender, age, mother tongue, region, education level and presence of children in the household in order to ensure a representative sample of the population. No margin of error can be associated with a non-probability sample (web panel in this case). However, for comparative purposes, a probability sample of 1,512 respondents would have a margin of error of ±2.52%, 19 times out of 20.

- Statistics Canada, “Canadian Perspectives Survey Series 1: Impacts of COVID-19 on Job Security and Personal Finances, 2020,” The Daily (April 20, 2020). Link: https://bit.ly/2Y9y42h.

- Leanne Findlay and Rubab Arim, “Canadians Report Lower Self-Perceived Mental Health During the COVID-19 Pandemic,” STATCAN COVID-19: Data to Insights for a Better Canada, Statistics Canada catalogue no. 45280001 (April 24, 2020). Link: https://bit.ly/2xMorvZ.

- Ibid.

Families New to Canada and Financial Well-being During Pandemic

Laetitia Martin

May 21, 2020

In 2015, the 193 Member States of the United Nations Organization, including Canada, adopted 17 sustainable development goals. Over a 15-year time frame, the plan aims to “end poverty, protect the planet and improve the lives and prospects of everyone, everywhere.”1 Eradicating poverty is ranked first because of the extreme vulnerability that it causes, especially in a time of crisis such as the pandemic that we are experiencing now.

Given this period of increased vulnerability, it is even more important to monitor the evolving economic situation and well-being of the most disadvantaged families. Whether one thinks of Indigenous, immigrant, single-parent or other types of families facing poverty, analyzing regularly updated data is vital to follow developments in the situation. In this way, our public decision makers will be able to implement effective policies and programs to reduce poverty, even in a time of crisis.

Based on data from the 2016 Census, almost 1 in 3 immigrant children (32.2%), one of the most economically vulnerable groups in the country, lives in poverty.2 What are the economic difficulties currently facing these families?

Three out of 10 immigrants had difficulty meeting their immediate financial obligations

In a time of pandemic, the entire population may experience financial losses, regardless of the prior level of economic vulnerability. Data collected during a recent survey conducted over a six-week period by the Vanier Institute of the Family, the Association for Canadian Studies and Leger show this clearly.3

Regardless of their immigrant status, nearly 4 to 5 out of 10 respondents stated that they had experienced a decrease in their income because of the pandemic. Immigrants were represented to a higher degree, however, among those for whom this decrease in income caused difficulty in meeting their short-term financial obligations (fig. 1). In the first weeks following implementation of social distancing measures, almost 3 out of 10 immigrants (29%) stated that they had difficulty paying their rent or mortgage due to the crisis. This was almost 1 out of 10 persons higher than their Canadian-born counterparts (20%). The gap appears likely to persist over the coming weeks.

Similarly, a greater proportion of foreign-born versus Canadian-born individuals experienced other short-term financial difficulties, such as paying bills on time. These financial stress indicators make the foreign-born population all the more vulnerable when they encounter difficulty meeting their basic needs, such as having a roof over their heads and accessing related public services, the minimum needed for their well-being and that of their family.

More than 1 out of 2 immigrant parents experienced a loss of income

Looking more closely at the economic impact of the crisis on immigrant families, one sees that the negative effects were immediate (fig. 2). In late March, more than 1 out of 2 immigrant parents stated that they had experienced a loss of income because of the pandemic, resulting in a reduced capacity to assist other family members financially. This support might not only have proven even more useful during this difficult time, but its decrease might also have a snowball effect within the most economically vulnerable ethnic communities.

Downward trends of immigrant parents experiencing immediate financial difficulties

On a more positive note, trends observed over recent weeks have shown a decrease in the proportion of immigrant parents who experienced immediate financial impacts. After reaching a high during the first week of April, the proportion of immigrant parents who had difficulty paying their rent or mortgage, as well as those who had difficulty meeting their other financial obligations, decreased by more than 15 percentage points in the following four weeks. While it is too early to determine the precise cause of the decrease, these results suggest that businesses that have adapted in an ongoing effort to maintain services despite distancing rules, coupled with the financial measures put in place by governments, may be helping lessen the economic vulnerability of immigrant families in the immediate term.

Financially vulnerable immigrant families visit the grocery store more often

Beyond direct financial impacts, economic vulnerability can also limit the ability to adopt certain behaviours that promote good health. For example, some parents of immigrant families may have to make difficult choices between the basic needs of their family and the resources they have to reduce their exposure to COVID-19. Furthermore, some economically vulnerable families do not have any credit cards to shop online, cannot pay the added cost imposed by grocery stores for delivery or packaging of items, or do not have the necessary financial resources to buy provisions to last them over several days. Not to mention that it might be more difficult for individuals without a car to transport a large amount of provisions on foot or on public transit.

These constraints might explain why twice as many immigrant parents who experienced immediate financial difficulties (46%) went to the grocery store more than once a week, compared with their Canadian-born counterparts, who had not experienced the same difficulties (23%) (fig. 3). No significant difference was observed between the two groups regarding compliance with other safety measures, such as social distancing and frequent hand washing, which suggests that this increased exposure cannot be explained by a lack of awareness.

In instituting sustainable development goals in 2015, the 193 States around the world recognized that “inequality threatens long-term social and economic development.”4 Often called a land of immigrants, Canada nevertheless remains a country in which immigrant families face a high risk of economic vulnerability. Data collected at the start of the pandemic show that inequalities persist in a time of crisis. Immigrants are harder hit financially in the immediate term than their Canadian-born counterparts.

Six weeks of collecting weekly data would seem to bear witness to a national resiliency or capacity to adapt to this extraordinary situation by mitigating certain negative effects. The downward trend in the prevalence of immigrant families that experienced difficulty paying their mortgage or rent, or meeting their other financial obligations, can be seen as a positive. But if the past weeks have taught us one lesson, it is that the situation changes rapidly in a time of pandemic. It is therefore more important than ever to closely monitor the situation and to be sure to identify, in a timely manner, the needs of the most vulnerable families, be they Indigenous, immigrant, single-parent or other. Eradicating poverty is an even greater challenge in a time of crisis.

Laetitia Martin, Vanier Institute on secondment from Statistics Canada

Notes

- United Nations Organization, “Sustainable Development Program,” Sustainable Development Goals. Link: https://bit.ly/35ZOi07.

- Statistics Canada, Data Products, 2016 Census, Data Tables, Statistics Canada catalogue no. 98-400-X2016206. Link: https://bit.ly/35Z1WAi.

- The survey, conducted by the Vanier Institute of the Family, the Association for Canadian Studies and Leger on March 10–13, March 27–29, April 3–5, April 10–12, April 17–19, April 24–26 and May 1–3, 2020, included approximately 1,500 individuals aged 18 and older, interviewed using computer-assisted web-interviewing technology in a web-based survey. All samples, with the exception of those from March 10–13 and April 24–26, also included booster samples of approximately 500 immigrants. Using data from the 2016 Census, results were weighted according to gender, age, mother tongue, region, education level and presence of children in the household in order to ensure a representative sample of the population. No margin of error can be associated with a non-probability sample (web panel in this case). However, for compahttps://bit.ly/3mQFdPdrative purposes, a probability sample of 1,512 respondents would have a margin of error of ±2.52%, 19 times out of 20.

- United Nations Organization, “Reduced Inequalities: Why It Matters,” Sustainable Goal #10: Reduced Inequalities. Link: https://bit.ly/3mQFdPd (PDF).

Families Struggle to Cope with Financial Impacts of the COVID-19 Pandemic

Jennifer Kaddatz

April 9, 2020

When it comes to personal and family finances, Canada as a whole has been hit hard by the COVID-19 pandemic. Early estimates indicate that more than 3 million people in this country have applied for the government’s emergency relief and Employment Insurance since March 16, 2020.

The financial downturn has been felt by virtually all families, many indicating that the financial stress is having an impact on their mood, mental health and sleep. People who have immigrated to Canada within the past 10 years and families with children and youth at home are among those most likely to say that they have been challenged financially as a result of the pandemic.

Families see coronavirus as a threat to their financial well-being

According to April 3–5, 2020 survey data1 from the Vanier Institute of the Family, the Association for Canadian Studies and Leger, more than half (53%) of adults aged 18 and older report that the coronavirus outbreak poses a major threat to their personal financial situation, while 36% view the crisis as a minor threat. In contrast, 11% of adults say that the outbreak is not a threat to their finances.

More than 7 in 10 (73%) recent immigrants to Canada (i.e. those who arrived in Canada in the past 10 years) report that their financial well-being is threatened by the pandemic in a “major” way. This compares with 58% of immigrants who came to Canada 10 or more years ago and half (50%) of those born in Canada (fig. 1).

Fig 1. Percentage of the population aged 18 and older who say that the COVID-19 outbreak is a threat to their personal financial situation, by immigrant status.

Adults who say that the pandemic poses a “major threat” to their financial situation commonly report “very often” or “often” feeling anxious or nervous (58%), feeling sad (56%) or having difficulty sleeping (44%) since the beginning of the COVID crisis. Families with children at home were the most likely to report heightened anxiety and reduced sleep (fig. 2).

What is particularly interesting among those who see the outbreak as a “major threat” to their financial situation is that parents of teenagers, rather than parents of younger children, most frequently report feeling anxious or sad “very often” or “often.” It is conceivable that this reflects parents’ concern about youth missing school, having to be home schooled, losing their jobs or work experience, and having an uncertain future with respect to a post-secondary education, in addition to concerns about the overall financial well-being of the family.

Fig. 2. Percentage of the population who view the COVID-19 outbreak as a “major threat” to their financial situation and who “very often” or “often” feel anxious or nervous, feel sad or have difficulty sleeping, by presence of children in the home.

Recent immigrants, low-income families and families with children are disproportionately impacted by income loss

Nearly half (45%) of people in Canada say that their income has decreased as a result of the COVID-19 pandemic. Income losses are impacting some more than others, however. For example, adults who had reported a total household income, before taxes, under $19,999 in 2019 are more commonly reporting lost income in 2020 as a result of the crisis, at 56%, compared with 37% to 48% of those in higher income groups.

A striking 7 in 10 (68%) recent immigrants say that they have had a decrease in income since the start of the coronavirus crisis, compared with about 4 in 10 earlier immigrants (45%) and Canadian-born adults (43%) (fig. 3).

Families with children and youth at home report a negative impact on their income more frequently than families without anyone under the age of 18 at home. Specifically, 54% of adults with children and youth living in their household indicate that at the moment the current crisis is having a negative impact on their income, compared with 41% of those without children.

Fig. 3. Percentage of the population aged 18 and older who report that their income has decreased as a result of the current crisis, by immigrant status.

Families report decline in retirement savings and other investments

Although decreases in total income due to job loss may have the biggest or most significant impact on families in Canada, the most prevalent negative financial impact of the COVID-19 pandemic has not been a loss of wages but rather a decline in retirement savings and other investments. More than half (54%) of adults report that their retirement funds or other investments have been impacted negatively since the current crisis started, and the proportion saying so increases with age (fig. 4).

More than 6 in 10 (63%) of those age 65 and older report a negative impact on their retirement funds or investments, as do 62% of 55- to 64-year-olds and 58% of 45- to 54-year-olds.

Negative financial impacts on retirement savings and other investments are likely just one of several factors influencing feelings of anxiety or nervousness since the beginning of the pandemic. Although 63% of those aged 65 and older reported that their savings are negatively affected, they in fact had the lowest share of those reporting increased anxiety or nervousness compared with other age groups who had experienced negative impacts on retirement and investments (fig. 4).

Fig. 4. Percentage of the population aged 18 and older who report that the current crisis has had a negative impact on retirement savings or other investments, by age and feelings of anxiety or nervousness.

Recent immigrants, young adults and families with children struggle to pay bills and rent or mortgage

Given losses in income and the value of investments, it is not surprising that nearly 3 in 10 adults in Canada say that the COVID-19 pandemic has already had a negative impact on their capacity to pay bills on time (28%) and 2 in 10 to cover their rent or mortgage (22%).

Just over half (51%) recent immigrants are having difficulty in paying bills on time in the current crisis. This compares with 30% of earlier arrivals and 25% of Canadian-born. Nearly half (46%) of recent immigrants say that the crisis has had a negative impact on their ability to pay their rent or mortgage (fig. 5).

Younger people are more likely than those over the age of 45 to report having difficulties in meeting their housing costs, with 31% of those under age 45 reporting difficulty in paying their mortgage or rent, compared with 24% of 45- to 54-year-olds, 17% of 55- to 64-year-olds and only 4% of those aged 65 and older.

About 3 in 10 adults (27%) with children under the age of 18 living in their household saying the COVID-19 pandemic poses challenges to their capacity to pay rent or mortgage, compared with 2 in 10 adults without children in the home. Those with young children, under age 12, were slightly more likely to report this difficulty, at 29%.

Fig. 5. Percentage of the population aged 18 and older who report that the COVID-19 crisis has had a negative impact on their capacity to pay bills on time or to pay their rent or mortgage, by immigrant status.

Not being able to pay bills, rent or mortgage may be having a considerable impact on the mental well-being of many people in Canada. More than 6 in 10 adults who can’t pay their bills (61%), rent or mortgage on time (63%) say that they have been feeling anxious or nervous “very often” or “often” since the beginning of the COVID-19 crisis (fig. 6).

Fig. 6. Percentage of the population aged 18 and older who report feeling anxious “very often” or “often” since the beginning of the COVID-19 crisis and report that the COVID-19 crisis had a negative impact on their capacity to pay bills on time or to pay their rent or mortgage.

Jennifer Kaddatz is a Senior Advisor at the Vanier Institute of the Family.

Note

- The survey included approximately 1,500 individuals aged 18 and older, plus a booster sample of 500 immigrants, interviewed using computer-assisted web-interviewing technology in a web-based survey. Using data from the 2016 Census, results were weighted according to gender, age, mother tongue, region, education level and presence of children in the household in order to ensure a representative sample of the population. No margin of error can be associated with a non-probability sample (web panel, in this case). However, for comparative purposes, a probability sample of 1,512 respondents would have a margin of error of ±2.52%, 19 times out of 20.

Modern Family Finances: Military and Veteran Families in Canada

Canada’s military and Veteran families are diverse, resilient and strong, and they make significant contributions to society as they manage their work and family responsibilities.

Research shows that military and Veteran families share many of the same financial stressors as civilian families, including changes in family income and/or employment, disruptions or unexpected expenditures (e.g. out-of-pocket medical expenses, foreclosures) and major life events (e.g. marriage, divorce, childbirth).

However, employment with the Canadian Armed Forces (CAF) brings with it the realities of military life, including a greater degree of mobility, separation and risk. These factors contribute to the uniqueness of military family life, and they can have a positive impact on family finances (e.g. benefits, relatively stable full-time employment and income), as well as negative impacts (e.g. costs associated with relocation and deployments, career sacrifices for partners of serving CAF members, difficulties for Veterans transitioning to civilian life and the civilian workforce).

This edition of Modern Family Finances explores military and Veteran families in Canada, focusing on the unique realities and experiences that impact their income and expenditures, savings and debt, and wealth and net worth.

Highlights include:

- In 2018, more than four in 10 CAF members (43%) reported having some financial problems, with 10% citing this as the most significant problem they faced in the past year.

- In 2018, among CAF members who had been posted to a new location, nearly six in 10 (57%) said that their financial situation had worsened, with a change in the cost of living cited as the main reason.

- In 2016, the Veteran population in Canada was less likely to be in the paid labour force (28%) than civilians (20%).

- In transitioning to civilian life, research shows that female Veterans experience a significantly higher average decline in income (a decline of 21% between their pre-release year and the first three years afterwards) than male Veterans (a decline of 1%).

- Research shows that in the workplace, Veterans are nearly three times more likely than the general working population to report having long-term physical or mental health conditions or a health-related activity limitation at work (35% and 13%, respectively).

Download Modern Family Finances: Military and Veteran Families in Canada

Research by Gaby Novoa and Nathan Battams

Source information available on the PDF version of this resource.

Facts and Stats: Working Seniors in Canada (2019 Update)

A growing number of seniors in Canada today are choosing to remain in – or return to – the paid labour market to manage their multiple financial responsibilities and, for some, to provide support to younger generations. As seniors and their families adapt their financial management strategies, expectations and aspirations in response to this ever-changing environment, they in turn are reshaping workplaces, Canada’s workforce, modern retirement and the economy at large.

To explore the relationship between seniors and family finances, we’ve created a fact sheet that gathers statistics from a variety of sources about seniors, their economic well-being and their evolving relationship with the paid labour market.

Highlights include:

- According to the 2016 Census, 1 in 5 seniors in Canada worked at some point in 2015, 30% of whom worked full-year and full-time.

- In 2016, the average retirement age in Canada was 63.8 years – a slow but steady increase from a low of 60.9 years in 1998.

- In 2017, surveyed Canadians aged 60 and older who worked or wanted to work were nearly split on the question of whether it was “out of necessity” (49%) or “out of choice” (51%).

- Nearly 3 in 10 surveyed working seniors surveyed in 2018 (28%) reported that they provide financial support to their children.

Download Facts and Stats: Working Seniors in Canada (2019 Update).

Facts and Stats: House, Home and Family Finances (2019 Update)

Home is at the heart of family life, the primary setting in which our family relationships are built and nurtured throughout our lives, and the stage on which so many of our family memories are created.

Our relationships with our homes are shaped by the evolving social, economic and cultural contexts in which we live, and where we choose to call home can change over time as we adapt our expectations and aspirations to these ever-changing environments.

To further explore the relationship between families and their homes, we’ve updated our House and Home in Canada fact sheet with new data, this time with a focus on family finances and home.

Highlights include:

- In 2016, median monthly shelter costs in Canada were $1,130 for owned households and $910 for rented households.

- In 2016, 16% of owned and 40% of rented households in Canada had monthly shelter costs considered not affordable.

- According to recent estimates, it now takes 13 years for a typical person aged 25 to 34 to save a 20% down payment on an average-priced home in Canada, compared with 5 years in 1976.

- Recent estimates show that a typical person would have to earn at least $22.40 per hour to be able to afford renting an average-priced two-bedroom apartment in Canada.

Download the House, Home and Family Finances (2019 Update) fact sheet.

This resource will continue to be updated as new research and data emerges (previous versions will be continually available on our fact sheets page).

Published on August 15, 2019

A Snapshot of Grandparents in Canada (May 2019 Update)

Canada’s grandparents are a diverse group. Many of them contribute greatly to family functioning and well-being in their roles as mentors, nurturers, caregivers, child care providers, historians, spiritual guides and “holders of the family narrative.”

As Canada’s population ages and life expectancy continues to rise, their presence in the lives of many families may also increase accordingly in the years to come. With the number of older Canadians in the workforce steadily increasing, they are playing a greater role in the paid labour market – a shift felt by families who rely on grandparents to help provide care to their grandchildren or other family members. All the while, the living arrangements of grandparents continue to evolve, with a growing number living with younger generations and contributing to family households.

Using newly released data from the 2017 General Social Survey, we’ve updated our popular resource A Snapshot of Grandparents in Canada, which provides a statistical portrait of grandparents, their family relationships and some of the social and economic trends at the heart of this evolution.

Highlights:

- In 2017, 47% of Canadians aged 45 and older were grandparents, down from 57% in 1995.1

- In 2017, the average age of grandparents was 68 (up from 65 in 1995), while the average age of first-time grandparents was 51 for women and 54 for men in 2017.2, 3

- In 2017, nearly 8% of grandparents were aged 85 and older, up from 3% in 1995.4

- In 2017, 5% of grandparents in Canada lived in the same household as their grandchildren, up slightly from 4% in 1995.5

- In 2017, grandparents who were born outside Canada were more than twice as likely as Canadian-born grandparents to live with grandchildren (9% and 4%, respectively), the result of a complex interplay of choice, culture and circumstance.6

Download A Snapshot of Grandparents in Canada (May 2019) from the Vanier Institute of the Family.

Battams, N. (2019). A snapshot of grandparents in Canada. The Vanier Institute of the Family. https://doi.org/10.61959/disx1332e

Published on May 28, 2019

1 Statistics Canada, “Family Matters: Grandparents in Canada,” The Daily (February 7, 2019). Link: https://bit.ly/2BnyyFO.

2 Ibid.

3 No comparator provided because this is the first time the question has been asked in the General Social Survey.

4 Ibid.

5 Statistics Canada, “Family Matters: Grandparents in Canada.”

6 Ibid.

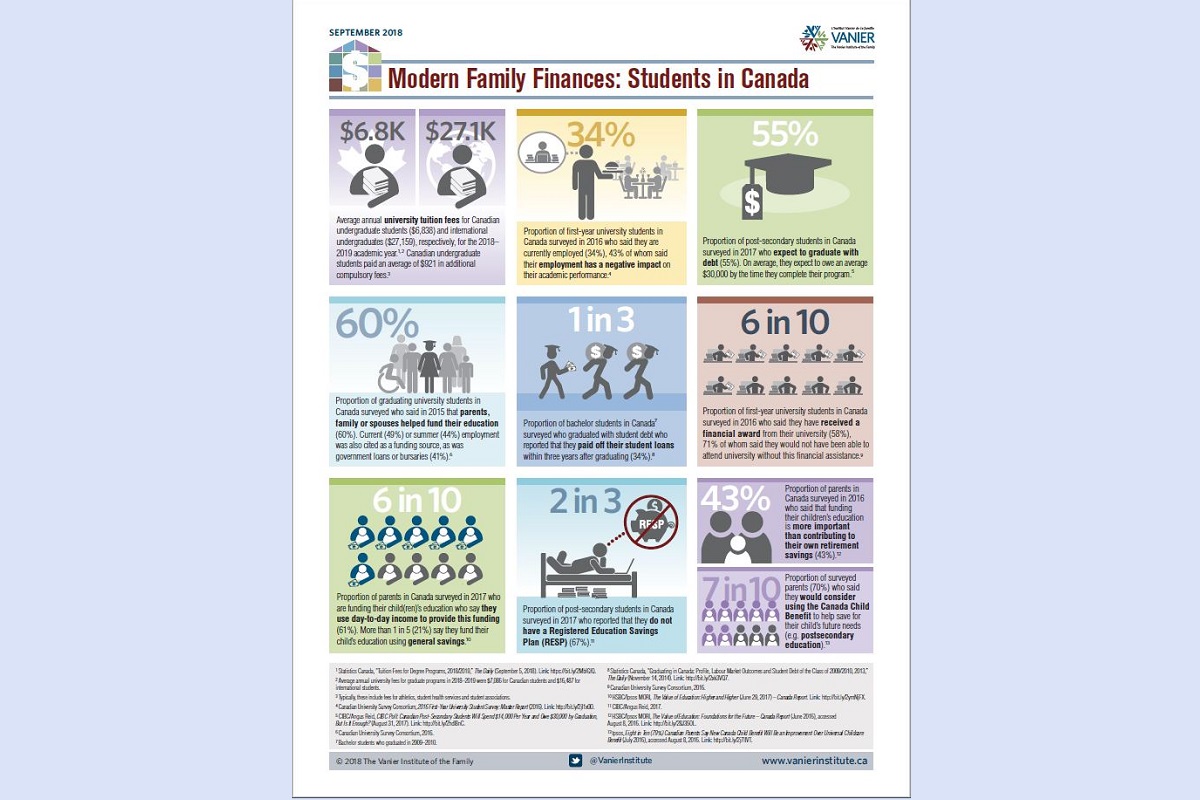

Modern Family Finances: Students in Canada (infographic)

Download the Modern Family Finances: Students in Canada infographic.

Post-secondary education is a family investment; regardless of who covers the costs, decisions surrounding higher education can have a significant impact on the lives of young adults and their families. A degree or diploma can open doors to employment and the possibility of higher earnings; however, higher education involves costs that must be managed, and families often play an important role in helping students manage their finances.

Using new survey information and data from Statistics Canada, the Vanier Institute has updated our infographic on students and family finances in Canada.

Highlights include:

- University tuition fees for Canadian undergraduate students were approximately $6,800 for the 2018–2019 academic year, with an additional $920 in additional compulsory fees.

- Six in 10 surveyed students reported that parents, family or spouses helped fund their education.

- Among surveyed parents who are funding their child(ren)’s education, 6 in 10 say that they use day-to-day income to provide this funding.

- Six in 10 surveyed first-year university students in Canada said they have received a financial award from their university, 71% of whom said they would not have been able to attend university without this financial assistance.

- One in three surveyed bachelor graduates who graduated with student debt reported that they paid off their student loans within three years after graduating.

Download the Modern Family Finances: Students in Canada infographic.

Work and Family: The Impact of Mobility, Scheduling and Precariousness

Elise Thorburn, PhD (Memorial University)

Download this article in PDF format

There is an immense shift underway in the workforce across Canada that is clear to many people who are working and to those who are looking for work. In recent years, there has been a rise in unstable and precarious employment, as well as a growing number of jobs with long commuting times and those involving long travel times during work. Furthermore, the use of shift-scheduling technology – which automates labour distribution in a workplace – is increasing across a variety of sectors. These evolving contexts can have a significant impact on workers and their families.

The use of shift-scheduling technology – which automates labour distribution in a workplace – is increasing across a variety of sectors.

A recent study conducted as part of the On the Move Partnership1 surveyed and interviewed union representatives and union members in Canada to explore how they manage unpaid family care responsibilities along with their often erratic work schedules and long or arduous commutes. The goal was to explore how these workers reconcile the rhythms of work and life in increasingly mobile and precarious sectors, and what unions are doing to foster harmony for these workers and their families.

Research from On the Move has shown that a large but difficult-to-document number of Canadians work in municipalities, provinces and even countries far from their homes and families, and their employment-related mobility often follows complex and nuanced patterns.2 These workers often invest considerable time and other resources managing and negotiating the impacts of this mobility.

This study focused on two particular types of mobility:

1. Lengthy and/or complex commuting, such as jobs that involve travelling an hour or more each way per day to the place of work (including the time it takes to drop off or pick up children, spouses, parents, etc.).

2. Mobility during/for work, such as jobs in which workers move around from worksite to worksite throughout the day, as with personal support workers or homecare nurses.

These categories aren’t exclusive; for some workers, these two categories – long commutes and mobility throughout the day – overlap. Study participants were all in the Greater Toronto Area, and they either worked in or represented employees within in the home health care sector, the airport and airline sector, or the higher education sector. While these workplaces differ greatly in the wages, skill sets and demographics of the workers, their diversity serves to highlight how the issues presented here can appear in different settings with different employee characteristics.

Unpaid idle time can represent “time taken from family”

One of the impacts of modern shift-scheduling practices and mobility is a greater amount of unpaid idle time for these diverse types of workers: time when they are not at home but not officially on the clock. Many of them referred to this as time taken from family, and it can have an impact on family finances. For example, if an employee was paying for child care but stuck with unpaid idle time, it could actually result in negative earnings. One airport worker, for example, recalled being scheduled for a shift that began at 2:30 a.m., but the last bus to leave from his neighbourhood to work left at midnight. Therefore, he regularly arrived at work an hour or more before his start time to ensure he was on time, and would then sleep or wait around at the airport – unpaid – until his shift began.

Home health care workers with long waits between clients also experience unpaid idle time, as reported by Kathleen Fitzpatrick and Barbara Neis.3The workers in their study were paid only for direct care time and the travel time between clients, regardless of how long they had to wait between scheduled visits. For example, one personal support worker said:

I start at 9:30 in the morning, work with a client for two hours, and then wait until 1:30 to see another client. When it’s not cold outside I sometimes sit on a park bench, but most of the time I find a Tim’s or a mall to sit in. I don’t have money to buy coffee at Tim Hortons every day while I wait for another shift to begin, but I am too far from home to go back there.

Her mobility between clients pulled her far from her home in her unpaid time, and for workers like her with children in daycare or with babysitters, that two hours of unpaid time between patients represented even greater negative earnings.

Aside from lost or negative earnings, idle time also represents unpaid time away from family. Some workers reported trying to resolve this lost family time by multi-tasking – for example, some parents of older children often “parent by phone” during long commutes, in idle time between clients or as they moved between worksites. One union representative in the home health care sector spoke of a member who texted constantly with her daughter throughout the workday. Another spoke of workers talking to their children about general life issues through meal preparation, homework and while commuting. During long commutes or drives between clients, the phone becomes a lifeline to more engaged parenting for many, helping to alleviate some of the stress of “leaving your children alone when you would not otherwise,” as one worker put it.

Aside from lost or negative earnings, idle time also represents unpaid time away from family.

University workers in the study reported that long commutes to rigidly scheduled classes can serve as time to catch up on sleep or to engage in preparatory work, reading or marking student papers. One university worker with a very young child, whose commute often stretched to more than 3.5 hours, said that the travel time by train was often the only time he could find to catch up on uninterrupted sleep. That said, he and other university workers also found that the long commutes and rigid schedules were the cause of significant mental health issues and troubled familial and social relationships.

Mobility and scheduling can affect employee and family well-being

The mental health ramifications of precarious work, as well as work with extended commuting and demands of child care, are well documented.4 The convergence of scheduling and mobility, paired with the responsibilities of family, had a negative impact on the mental health and well-being of interviewed university workers (e.g. stress, fatigue, anxiety). One said that his mental health was severely impacted by the pressures of the commute and the schedule, causing things at home to become “bad.” He noted, “I was feeling so very desperate earlier in the fall, even just seeking therapy became difficult.” The convergence of scheduling, onerous mobility and family care responsibilities made finding the time and energy needed to manage his mental health was an insurmountable task. The schedule and commute mitigated the rejuvenating aspects of his work, and he said exhaustion was very common by the end of the term. As well, maintaining his social circle outside of his immediate family was almost impossible and, he noted, “It [took] intense planning to even schedule a haircut.”

Accessing child care – quality, affordable child care that works for non-traditional schedules – is a major issue for mobile workers.

Another university and union worker noted that the time spent on transit exacerbated exhaustion and made the transition for children from daycare or school to home that much more fraught. “You are tired and cranky, and so is your child,” she said, and “you are never really able to honour the schedule of your child or yourself, which leads to you feeling guilty and just bad.” The need to always be up early and rushing to a long and onerous commute also caused her to have residual anxiety issues – issues she says stayed with her long after she left that particular job. “I always feel like everything is being done at the last minute and I’m constantly anxious about that,” she explained. The anxiety that she felt had an effect on her children, she believed, giving them their own sense of urgency or anxiety, and the feeling that the adults around them – those that are caring for them – are constantly in a state of heightened stress. This mirrors what Stephanie Premji found in her research on precarious immigrant workers in Toronto – the worry about work-related economic insecurity caused the children of these precarious workers to become depressed and it contributed to familial stress.5

Other union representatives and workers I spoke to also noted that family responsibilities and mobility paired with schedules that are out of one’s control increased their unpaid caring labour in the home, which in turn contributed to social isolation and the loss of support networks. They also spoke of their frustration in being unable to address or alter the situation they felt trapped in – they could not move closer to their workplace because it may often change, for example, or because they could not afford to live in areas with better employment opportunities. Other On the Move researchers have found that many aren’t able to overcome these barriers and improve their labour market experiences (and hence mental health) over time.

Non-standard work hours often don’t align with child care availability

All of the worksites in this study operate on non-traditional, often 24-hour schedules. Non-standard work hours include a variety of now-common schedule possibilities and working patterns – from slightly extended hours (beginning from 6 a.m. and ending around 7:30 or 8 p.m.) to later shifts (e.g. those that last until 11 p.m. or later) as well as full overnights and weekends.6

Non-standard hours of work have been steadily increasing in Canada, and Statistics Canada reports that the period from 2005 to 2015 saw a growing shift from traditional to more flexible, non-standard work schedules.7 Yet both transit systems and child care centres have been set up to meet the needs of a standard 9-to-5 work schedule, and have done little to change over this same time period. Many of the interviewed workers and union representatives said that the standard hours of transit and child care conflicted with the rhythms of their workplaces, meaning that daycare centres – formal, regulated and licensed to ensure quality and safety – were not an option for them.

Accessing child care – quality, affordable child care that works for non-traditional schedules – is a major issue for mobile workers. For many low-income, precarious workers on non-standard schedules, informal child care providers are the only accessible option. Such providers may be available by negotiation at a moment’s notice and during non-traditional hours, leading to situations of “trickle-down precarity.” These workers may also supplement child care providers with occasional help from family, friends and neighbours, or rely entirely on them – one union representative and worker at Toronto Pearson International Airport noted that his wife’s parents moved into their home for five years to care for their young children while he and his wife worked non-standard schedules for an airline.

For many immigrant workers, the social support systems they may have had in their home countries are absent, and thus accessing child care becomes a significant source of anxiety.

However, this reliance on family is not an option for everyone. For many immigrant workers, the social support systems they may have had in their home countries are absent, and thus accessing child care becomes a significant source of anxiety, especially as mobility and scheduling disrupt the rhythms of necessary care work in their home.8 Even with formal child care, long commutes and worker mobility paired with unpredictable or non-standard schedules can have emotional and mental health impacts on workers who engage in unpaid caring labour at home. One worker noted that her schedule and commute paired with traffic meant she was often arriving very close to the daycare’s closing time and, she noted, “There is the horrible shame of being the last person to pick your kids up.”

This was especially acute for women workers, who felt that their tardiness to collect children from care was a reflection of their quality as a parent. This shame and even fear is not entirely unwarranted: while most daycares have fines for picking children up after closing time – often in the range of $1 per minute – in 2016, a daycare in Etobicoke, Ontario instituted fines as high at $300 per hour, as well as a possible call to Children’s Aid Society if no parents or emergency contacts could be reached.9

One worker noted that punitive measures such as these are an enormous source of stress for her as she commutes between worksites on the subway, because while underground she has no cellphone access. She continually fears a subway delay or breakdown, since she would not be able to call and alert the daycare if she was going to be late. For her, this is a source of anxiety and stress that does not end when her commute does, but that carries with her into her interactions with her children and at home. Thus, to add to the sense of shame, anxiety and stress associated with mobility, family and non-standard schedules, the possibility of losing access to one’s children entirely is introduced, as well as the potential complication to immigration applications if Children’s Aid Society is ever involved.

Non-standard work scheduling can be complex and time-consuming

The challenges of non-standard work schedules, mobility and limited incomes, and the friction between schedules and child care, means that workers often spend unpaid time outside of work scheduling and coordinating work and family responsibilities, which further encroaches upon family time. In her research on call centre workers in Quebec, Karen Messing found that parents made use of eight different babysitting resources to fill caregiving needs over a two-week period, and spent considerable unpaid leisure time trying to switch shifts with co-workers to make up for the rest.10

When some workers cannot harmonize their schedules, commutes and family responsibilities, the only option may be to take fewer shifts or remain in casual positions – even if they are entitled to a full-time or permanent job.

When some workers cannot harmonize their schedules, commutes and family responsibilities, the only option may be to take fewer shifts or remain in casual positions – even if they are entitled to a full-time or permanent job. Some union representatives said their members in the home health care sector, for example, “choose” to remain in more precarious positions, because family life simply cannot be coordinated around work life. But as one mentioned, “It’s a tricky thing to say when it’s a choice and when it’s an obligation.” Another union representative said, “I’ve seen people quit entirely over this,” and reiterated that if not quitting, remaining casual was often a way that workers sought to assert more control over their work schedule and life.

Questions remain on mobility and the “duty to accommodate”